Medicare Part C

Medicare Advantage Plans

Medicare Part C, commonly known as Medicare Advantage, includes health plans offered by private insurance companies that are approved by Medicare. These companies must follow Medicare's rules and guidelines.

A Medicare Advantage plan bundles your Medicare Part A (Hospital Insurance), Medicare Part B (Medical Insurance), and often Medicare Part D (Prescription Drug Coverage) into a single comprehensive plan.

While you are still enrolled in Medicare when you join an Advantage plan, it is the private insurance company — not Medicare — that pays your healthcare claims.

Medicare pays the insurance company to manage your benefits.

All Medicare Advantage plans are required to provide at least the same level of coverage as Original Medicare (Parts A and B), and many plans offer additional benefits not available through Original Medicare.

Key Facts About Medicare Advantage Plans (MA Plans)

You must be enrolled in both Medicare Part A and Part B and continue paying your Part B premium. Out patient care at clinics or hospitals

You must live within the plan’s service area to be eligible.

You cannot be enrolled in both a Medicare Advantage plan and a Medicare Supplement (Medigap) plan at the same time.

Enrollment and disenrollment are only allowed during specific times of the year (such as the Annual Enrollment Period).

Insurance companies offering Medicare Advantage plans receive direct payments from Medicare to manage your healthcare needs.

Plans cannot base their pricing on your age, health status, or claims history.

Every Medicare Advantage plan must be annually reviewed and approved by the Centers for Medicare & Medicaid Services (CMS) before it can be marketed during the Medicare Annual Enrollment Period (AEP).

Out-of-pocket costs vary between Medicare Advantage plans; some plans may offer lower costs for certain services.

Understanding Medicare Advantage Plans

When you enroll in a Medicare Advantage plan, you will usually need to receive care from healthcare providers who are within the plan’s network. Some plans offer out-of-network coverage, but your out-of-pocket costs may be higher for those services.

Important Notes About Medicare Advantage Costs and Coverage:

Medicare Advantage plans may have higher or lower out-of-pocket costs depending on the services you use.

Home health care services (when medically necessary)

Annual Notice of Coverage (ANOC): This letter outlines changes to your coverage, costs, and service area for the upcoming year. Plans must mail it to you by September 30.

Evidence of Coverage (EOC): This document provides detailed information about what your plan covers and how much you will pay. You’ll receive a notice (or printed copy) by October 15, with instructions for accessing the EOC electronically or requesting a printed version.

Choosing the Right Medicare Advantage Plan:

Many healthcare providers accept only a limited number of Medicare Advantage plans.

Before enrolling, it’s important to confirm that your preferred doctors, specialists, and hospitals accept the Medicare Advantage plan you are considering.

Need Help? Spartan Health Plans is here to assist you!

Call our Helpline toll-free at 702-919-4844 to speak with a licensed insurance agent specially trained to help you understand your Medicare options.

Or request assistance online at: /speak-with-an-agent

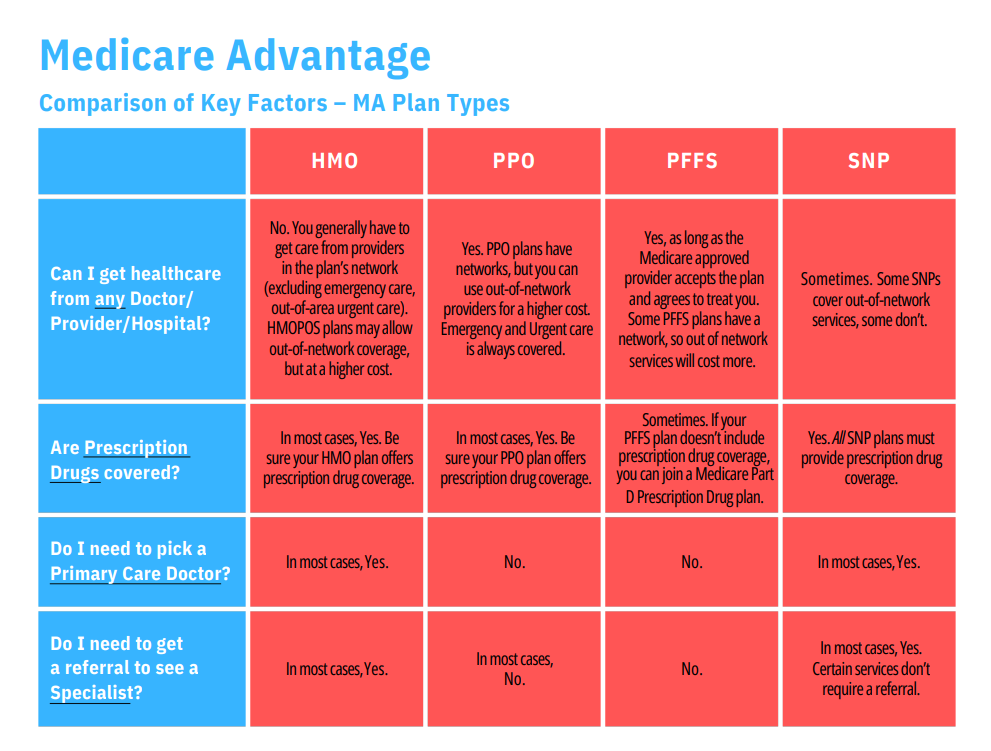

Types of Medicare Advantage Plans

Medicare Advantage offers several plan types, each designed to meet different healthcare needs and preferences:

Health Maintenance Organization (HMO) Plans

HMO plans typically require you to receive care from doctors, hospitals, and providers that are part of the plan’s network, except in emergencies.

You must usually live or work within the plan’s service area to be eligible.

If your doctor leaves the network, the plan will inform you, and you’ll need to choose another in-network provider.

Care received outside the network (non-emergency) usually means you pay the full cost.

Some services require prior authorization.

For more details, contact your HMO plan directly.

HMO Point-of-Service (HMOPOS) Plans

These plans are a hybrid version of HMOs and allow limited out-of-network care at a higher cost.

You often don’t need a referral to see specialists.

In-network (HMO) and out-of-network (POS) services have separate deductibles and separate out-of-pocket limits.

The deductibles and limits are not combined; they must be met separately.

Preferred Provider Organization (PPO) Plans

PPOs contract with a network of preferred providers, but you can see any doctor or hospital, in or out of network.

Using in-network providers usually costs less.

No referral is needed to see a specialist.

No requirement to choose a primary care doctor.

PPO networks are typically larger than HMO networks.

Private Fee-for-Service (PFFS) Plans

PFFS plans determine how much they will pay for services and how much you’ll owe.

Plan details, including costs, are outlined annually in the ANOC and EOC documents.·

Some PFFS plans have a network of providers who agree to treat you.

Out-of-network providers may refuse to treat you, even if they have seen you before (unless it’s an emergency, where treatment must be provided).

Special Needs Plans (SNPs)

SNPs are designed for individuals with specific healthcare needs or limited incomes. These plans tailor their benefits, provider networks, and drug coverage to fit special populations, including:

I-SNPs: Individuals who live in nursing homes or need in-home nursing care.

D-SNPs: Individuals eligible for both Medicare and Medicaid.

C-SNPs: Individuals with chronic or disabling conditions (like diabetes, ESRD, HIV/AIDS, heart failure, or dementia).

SNPs offer targeted benefits, including care coordination services.

Medical Savings Account (MSA) Plans

MSA plans combine a high-deductible health insurance plan with a special bank account set up by the plan.

The plan deposits money into the account, which you can use to pay for medical expenses throughout the year.

The amount deposited is usually less than the deductible.

MSA plans do not include prescription drug coverage; you’ll need to enroll separately in a Medicare Part D Prescription Drug plan if you want medication coverage.

Why Are Medicare Advantage Plans So Popular?

Medicare Advantage (MA) plans have become a popular choice for many Medicare beneficiaries for several reasons:

Prescription Drug Coverage: Most Medicare Advantage plans include prescription drug benefits (Part D), although not every plan offers this feature.

Out-of-Pocket Maximum: Unlike Original Medicare, Medicare Advantage plans have an annual limit on out-of-pocket costs for Medicare-approved services, providing financial protection.

Extra Benefits: Many plans offer additional benefits beyond Original Medicare, such as:

Routine vision exams and eye wear.

Preventive dental care.

Access to "ask-a-nurse" services.

Transportation assistance.

Mail-order pharmacy programs.

Gym memberships and wellness programs.

Pre-Existing Conditions Accepted: You can enroll in a Medicare Advantage plan even if you have a pre-existing health condition.

Important Reminder:

Medicare Advantage benefits can vary widely by plan, so it’s important to carefully review the Summary of Benefits for any plan you’re considering.

Questions About Medicare Advantage Coverage

What if I Have Other Insurance Coverage?

In some cases, enrolling in a Medicare Advantage Plan could cause you to lose your employer or union health coverage not just for you, but also for your spouse or dependents and you may not be able to get it back.

In other cases, you may be able to keep your employer or union coverage and use it alongside your Medicare Advantage Plan.

Some employers or unions also sponsor their own Medicare Advantage retiree health plans.

How Can I Find Out What’s Covered?

You can request an advance decision from your plan to confirm if a service, prescription drug, or supply is covered. This is known as an "organization determination".

Prior authorization may be required before coverage is approved.

You, your representative, or your doctor can request an organization determination.

If needed for urgent health reasons, you can request a fast decision.

If your plan denies coverage, they must notify you in writing, and you have the right to appeal.

If your plan refers you to a service or provider outside the network without prior authorization (called "plan-directed care"), you generally won’t have to pay more than the normal in-network cost sharing.

Check with your plan for specific details about these protections.

Do All Medicare Advantage Plans Include Prescription Drug Coverage?

In most cases, yes — Medicare Advantage plans typically include Medicare Part D prescription drug coverage.

However, some plans, such as MSA plans and certain PFFS plans, either cannot or choose not to offer drug coverage.

If your Medicare Advantage plan does not include drug coverage, you can enroll in a stand-alone Medicare Part D plan.

Important: If you are enrolled in an HMO, HMOPOS, or PPO Medicare Advantage plan and you separately enroll in a stand-alone Medicare Part D plan, you will be disenrolled from your Medicare Advantage plan and returned to Original Medicare.

Questions About Medicare Advantage Coverage

What if I Have Other Insurance Coverage?

- In some cases, enrolling in a Medicare Advantage Plan could cause you to lose your employer or union health coverage not just for you, but also for your spouse or dependents and you may not be able to get it back.

- In other cases, you may be able to keep your employer or union coverage and use it alongside your Medicare Advantage Plan.

- Some employers or unions also sponsor their own Medicare Advantage retiree health plans.

How Can I Find Out What’s Covered?

- You can request an advance decision from your plan to confirm if a service, prescription drug, or supply is covered ("organization determination").

- ✓ Prior authorization may be required before coverage is approved.

- ✓ You, your representative, or your doctor can request it.

- ✓ If urgent, you can request a fast decision.

- ✓ If denied, you must be notified in writing and have the right to appeal.

- ✓ If referred to an out-of-network provider without prior authorization, you generally won’t pay more than the in-network cost.

Check with your plan for specific details about these protections.

Do All Medicare Advantage Plans Include Prescription Drug Coverage?

- ✓ In most cases, yes — Medicare Advantage plans typically include Medicare Part D prescription drug coverage.

- ✓ Some plans (MSA, PFFS) may not offer drug coverage.

- ✓ If drug coverage is not included, you can enroll in a stand-alone Medicare Part D plan.

- Important: If you are in an HMO, HMOPOS, or PPO Medicare Advantage plan and enroll in a stand-alone Part D plan, you will be disenrolled and returned to Original Medicare.

Copyright © 2012–2025 Powered by SBI Benefits. All Rights Reserved

Disclaimer | Privacy Policy | Sitemap Mailing Address:

We do not offer every plan available in your area. We currently represent 20 organizations offering 56 products. For a complete list of options, contact Medicare.gov, 1-800-MEDICARE, or your State Health Insurance Program (SHIP). By submitting your contact information, you consent to receive marketing communications from Spartan Health Plans, including calls and texts (automated, AI-generated, or pre-recorded). Message and data rates may apply. Consent is not required for enrollment and can be withdrawn at any time, even if your number is on a Do Not Call list.